In its Q1 2024 earnings report, Amazon shared that it's on track to be profit making internationally for the first time since the pandemic lockdowns lifted.

The Financial Times views this achievement as a permanent shift to profitability internationally, achieved by continuous growth in its advertising business, along with a shift of learnings from North America to the EU. A big driver of profitability is efficiency in its largest markets, UK and Germany, where delivery speed has increased and cost to serve has decreased. Amazon noted on a recent earnings call how customers will shop new categories as they discover the fast shipping options – Fast Moving Consumer Goods (FMCG).

But Amazon’s regular mention of improved supply chain efficiency has vendors wondering – if things are better, where are my purchase orders?

Weeks of cover (WOC) is considered an important metric to understand the health of your stock levels at Amazon – as items fall below about 2-4 weeks of cover, you are at risk of going out of stock, and Amazon places a purchase order to ensure inventory is enough to cover more weeks of sales.

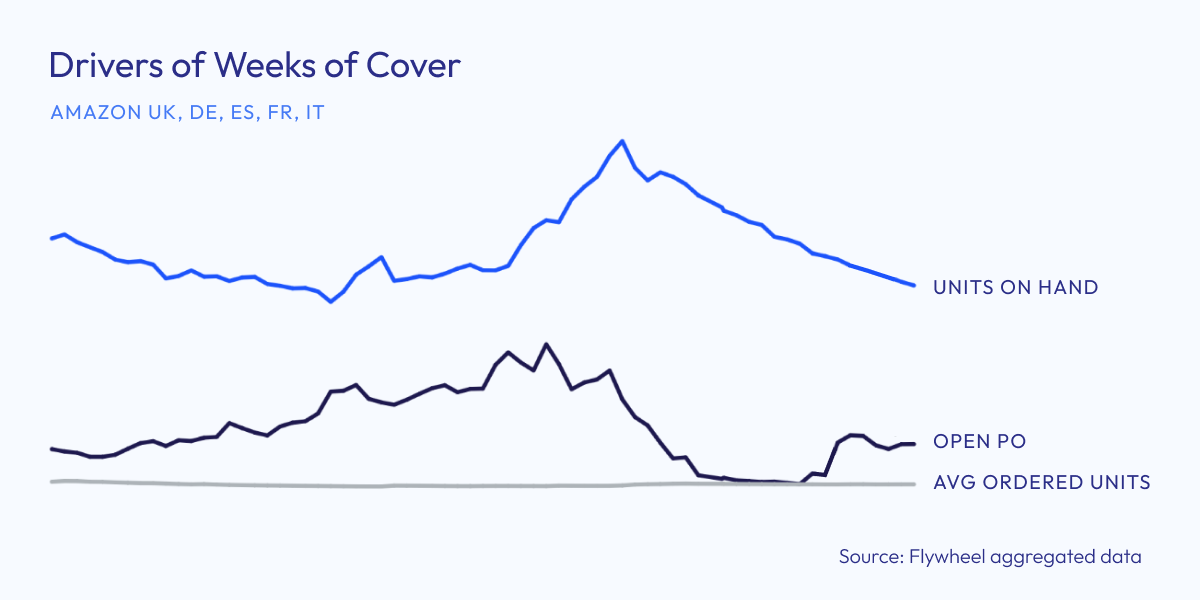

Across the UK and EU5 (UK, Germany, France, Italy and Spain), WOC has seen a steady decline since its peak in November for Cyber Week. After this promotional event, Amazon all but halted its ordering to reduce the total units on hand.

In the plot above we can see how the number of units in aggregate purchase orders has fallen (black line), leading to fewer units on hand at fulfilment centres (blue line).

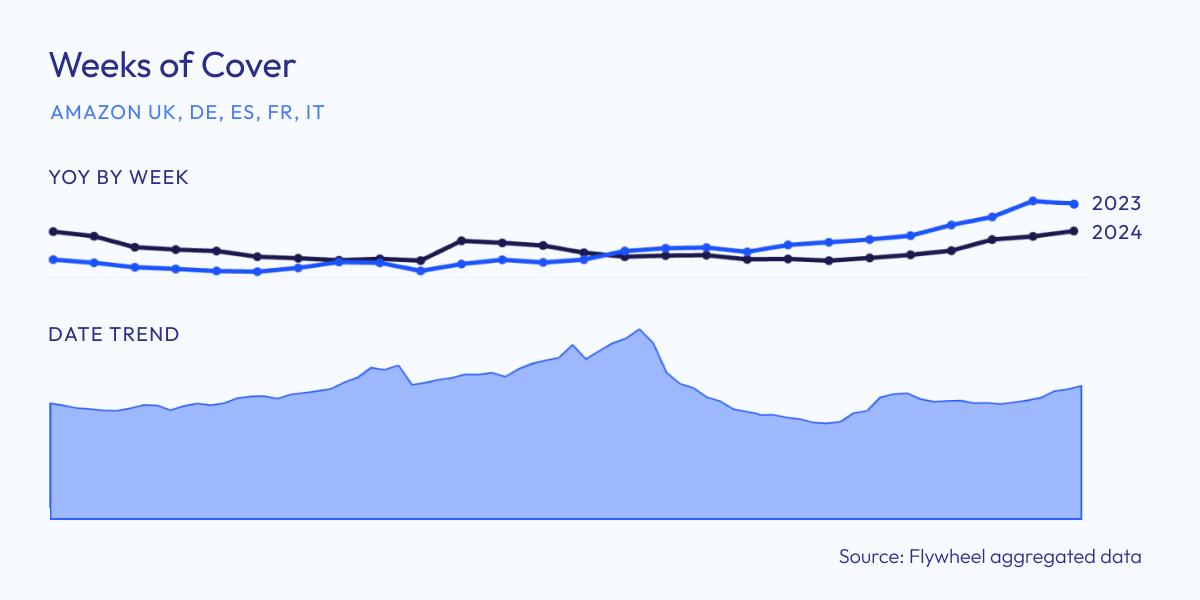

The chart above shows us weeks over cover, by week, year to date.

To show this is not just a seasonal trend, we look at the year-over-year trend and see that in the last 13 weeks, weeks of cover has declined by 7% YoY.

Weeks of cover dropped below 2023 levels for the first time in April of this year, and has steadily declined ever since. Despite open POs increasing from March onwards (as seen in our first chart), WOC has now remained steadily lower than 2023 levels.

But not all categories are equal: while WOC is down 10% YoY for hardlines and 5% YoY for softlines, WOC has actually increased by 10% for FMCG.

Why is this happening?

A focus on efficiency

While measures of sellout to consumers (in the form of Shipped COGS and Ordered Revenue) have remained high, sell in to Amazon has declined, leaving businesses struggling to hit internal sell in targets.

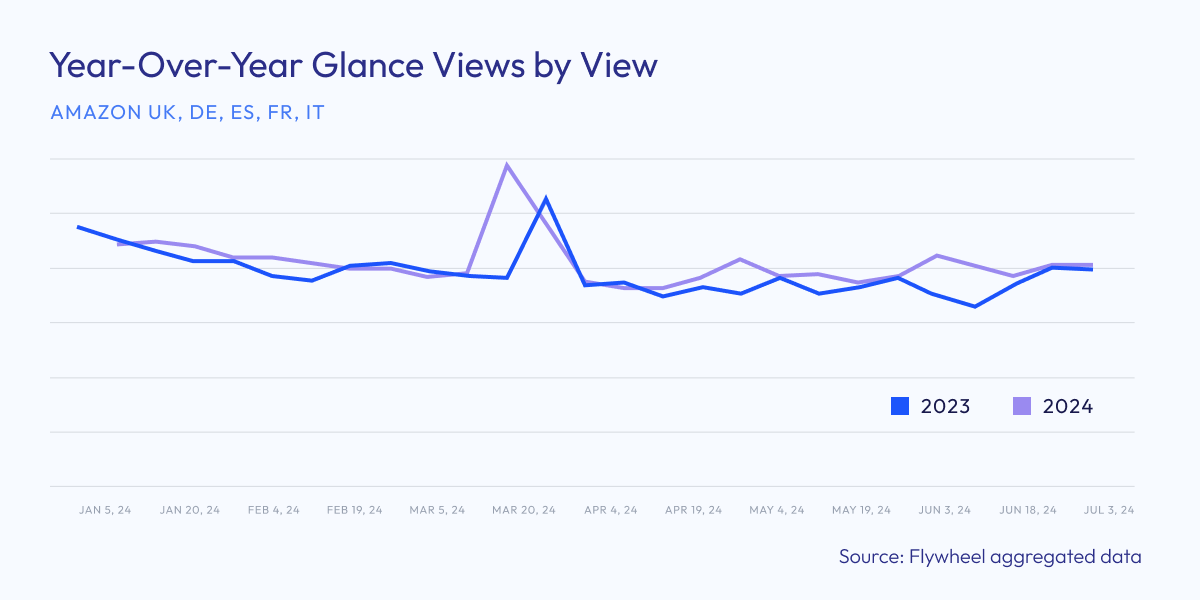

This rebalancing is no surprise, however, as WOC in the EU is significantly higher than the US. In its Q1 earnings report, Amazon stated clearly that it’s taking the learnings from the US and applying them to the European market. “We're following a similar trajectory as North America in terms of benefiting from regionalization shift, and we saw that average distance of each package traveled actually came down by 25 kilometers.” Consumers are receiving packages faster than ever before, which is building loyalty to Amazon as an established channel within the shopper journey and leading to higher traffic. The data agrees with this assessment: across the EU, glance views are up 6.2% YoY.

In some ways, the decrease in stock held at Amazon can be seen as an advantage: There’s a lower risk of stock expiration and returns to vendors from Amazon. However in the short term, vendors are feeling the strain of lower sell in rates, particularly if they make advertising budget decisions based on sell in rather than sellout.

And the increased efficiency is coming with some cost: we looked at the top 20 SKUs in every geography, and availability rates have decreased dramatically, from 64% in 2023 to 56% in 2024. If that’s the case, how is Amazon continuing to accelerate sales?

A focus on the right SKUs

Just as you look at your assortment and decide where to invest more, let it coast, or exit, Amazon too is evaluating your portfolio and making some decisions on where to play.

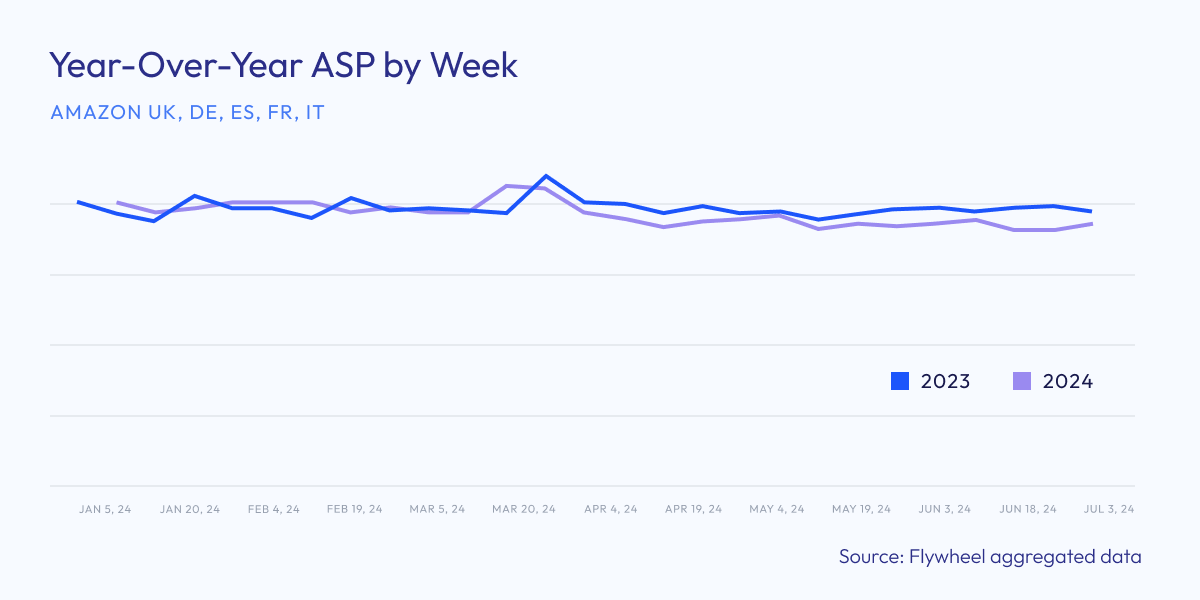

Historically, Amazon has pushed for greater profitability, which usually means a focus on higher priced SKUs where the margin is greater. Where the Average Selling Price (ASP) is lower, the cost to ship the product is proportionally larger, which leads to lower profitability and risk of Amazon refusing to stock your product – an action that, depending on how long you’ve been working on Amazon, you might affectionately call CRaP, ROO, or another acronym of your choice.

Now, because of the increased efficiencies Amazon has gained, we notice Amazon is shifting to lower priced SKUs instead. With 33% of vendors reportedly increasing cost prices in 2024, you would expect ASP to increase. But we’ve seen the opposite is true – ASP has decreased by 1.7% in 2024.

Source: Flywheel aggregated data

Amazon has created a virtuous cycle. By investing in its supply chain, Amazon has decreased cost to serve and increased shipping speed. This has allowed it to list more FMCG items while at the same time, customers, driven by macro economic issues like inflation, have pulled back on discretionary items and spent more share of wallet on FMCG, where Amazon has a unique price, selection, convenience and now speed advantage (with the exception of frozen and refrigerated grocery).

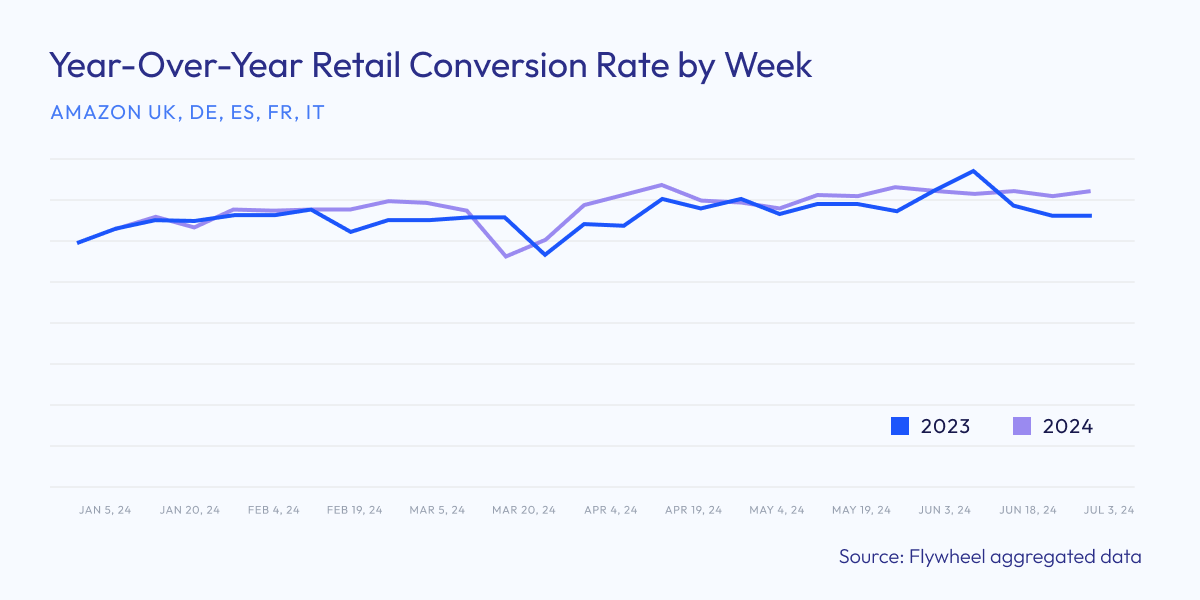

Conversion data shows us that consumers are more willing to purchase: along with the increase in glance views, conversion rates have increased by 3.1% this year. This is driven by both quick shipping and a mix shift to FMCG, where the aggregate conversion rate is higher than hard lines.

Amazon needs to offer the items consumers are looking for, and often the first point of entry to Amazon is a low-cost item. Recognising this, Amazon can use its newfound efficiency – and your higher negotiated vendor terms – to support the items that it views as critical to various categories. This was a lesson they learned in the pandemic: if category leading SKUs went out of stock, customers would leave Amazon and go to other retailers. As such, Amazon is willing to compress profitability on these key SKUs.

A look across the pond

Interestingly, the US is not seeing the same, as Amazon maintains about 4-6 weeks of cover as its baseline. But as we learned from the Financial Times, the efficiency achievements have already occurred in the US – their rebalancing actually happened in 2022, and vendors had a similar scare.

According to Cleveland Research Company, US vendors are managing their own challenges, in particular volatile ordering patterns and shorter Vendor Lead Times as Amazon consolidates and reconfigures its warehouses.

But allow this to give us all some confidence: If the earnings report and the US’ success after its own rebalancing are any indication, EU vendors will continue to see growth, despite this temporary decline in purchase orders.

Key Takeaways

If lower sell in figures are causing turmoil within your business, it’s time to reframe the conversation:

This is a rebalancing in 2024, caused by greater supply chain efficiencies and a reduced need for high WOC. This is not an indicator of risk that Amazon is in decline, as it’s more a one-time reduction spurred by Amazon’s order and fulfilment efficiency. In fact, Amazon continues to experience an increase in demand, evidenced by continuous growth in consumer ordered revenue.

Consumers are receiving orders faster than ever before, which builds loyalty and affinity to the channel.

Sales (both shipped COGS and ordered revenue) continue to grow. More than ever, Amazon is able to support the best SKUs in your assortment.

Demand is the best indicator of success, and should be used to justify continuous investment in Amazon.

Amazon’s performance gives us clear signals: It is in one of the healthiest positions internationally that it’s ever been in before. Its focus on greater efficiency has satisfied consumer needs, and we can expect this health to translate into continuous sales growth in future months and years.

Are you impacted by this trend? If you’re a Flywheel client, reach out to your account team today – we can provide support and help you understand what you can do to adjust strategy according to Amazon’s changing ordering patterns. If you're not a Flywheel client, our experts can help you learn more about what these changes mean for your business. Start a conversation today!

Ready to grow your business?

Let's discuss the best approach to meet your brand's specific needs.

Let's connect